September 2023 Labor Market & Economy Report: Job Growth Shows Off Economy's Spooky Resilience

The economy doesn’t stop.

It can only be slowed down and typically not for very long. Unless some extraordinary force shocks it deeply. Even then it always comes back, stronger than ever.

Explained in Halloween terms, our economy is a lot like Michael Myers.

Not in the evil sense, of course. But in the unrelenting sense. Both have the uncanny power to press on despite being hit by a kitchen sink or two.

The comparison feels especially cogent right now, given the Bureau of Labor Statistics announced that 336,000 new jobs were created in September -- double what was predicted (that’s on top of a revision that added 119,000 jobs to July and August totals).

Didn’t this economy absorb eleven interest rate hikes in 18 months?

It did, yet it won’t relent.

Unemployment, unchanged at 3.8% in September, remains historically low, indicating there’s still a big need for workers.

Consumer spending has also been strong, buoyed by a population with disposable income rooted in a combination of savings, stimulus money, and, at least so far in 2023, a steady increase in real hourly compensation.

However, continued job growth, a tighter labor supply, and consumer spending will theoretically work against taming inflation. On that note, inflation in September stayed at 3.7% year-over-year, unchanged from August, and not any closer to the ideal soft-landing spot of 2%.

On the flip side: job growth, labor demand, and consumer spending are credited with keeping us from entering a recession; a recession that hasn’t happened despite stricter lending, constrained borrowing, and dampened market outlooks. A bond yield curve inversion says one thing, but the economy, so far, says another.

Anyone in favor of a soft landing is okay with where things stand. The hope is current interest rates are enough to keep chipping away at inflation, albeit gradually.

The Fed meets November 1 and is expected to leave interest rates unchanged for now.

The bad news is the soft-landing balancing act will continue into 2024, meaning interest at current rates, and the headwinds that come with them, will continue to be economic realities.

What to watch for...

Unlike Michael Myers, the forces sustaining our economy are not supernatural; we know what they are. We’re just not entirely certain always which force is impacting what, or how much, and when.

Among those forces, government stimulated growth and demand has certainly played a large role.

Federal spending, including economic investments (Infrastructure Investment and Jobs Act, Chips Act, and Inflation Reduction Act), social benefits, and unemployment assistance, soared since 2020. It’s currently 33% above what was spent in 2019.

Why bring it up?

Federal spending typically lives at the heart of long-standing national debt debates and re-occurring government shutdown battles in Congress, including the most recent in September. In dramatic fashion, a shutdown was temporarily averted under an agreement that allotted funding until Mid-November.

If a shutdown were to happen in November, it’s likely to cause pain but unlikely to have a significant impact on the relationship between federal spending, national debt, and our economy, which for decades has grown substantially bigger and more complex.

Since 1970, overall federal spending has increased twenty-seven-fold, while Gross Domestic Product (GDP) has increased twenty-five-fold.

The gap between GDP and federal spending has also gotten smaller. In 1950, GDP outpaced spending more than 6 to 1. In 1970 it was just under 5 to 1. By 1990, it was 4.6 to 1. In 2010, following the Great Recession, it went from 4.6 to 3.9 to 1. In 2020, during the pandemic, it reached 3.1 to 1, the lowest it’s been in 70 years.

Currently, the GDP to Federal Spending ratio is 4.2 to 1.

Thus, the goods and services the federal government directly purchases have steadily become a bigger component of our Gross Domestic Product (GDP) over the years. Indirectly, so has the money the government re-distributes into the economy in the form of stimulus and benefits, which people use to purchase products and services with, which also impacts GDP.

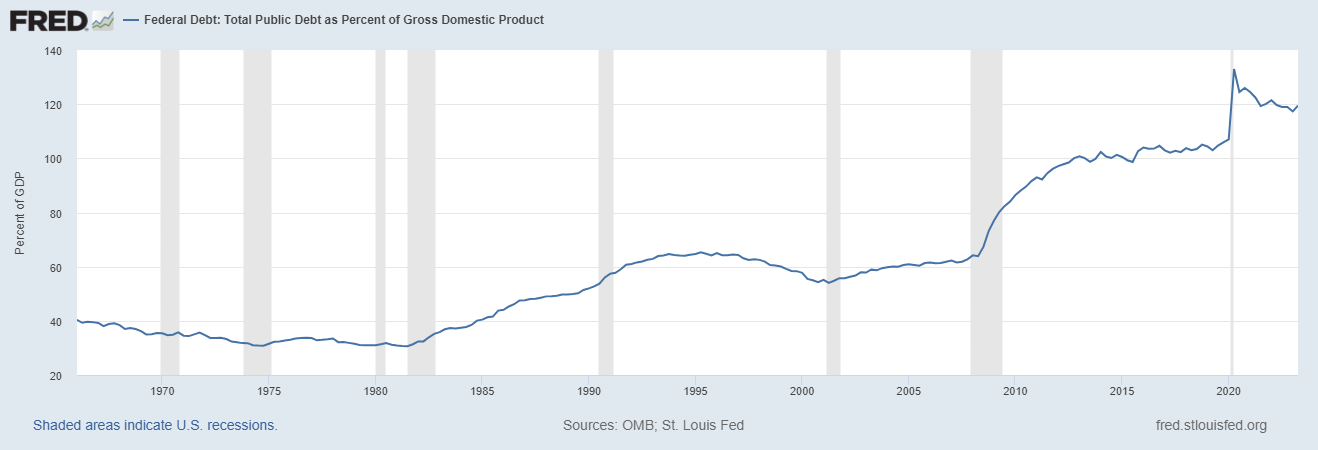

The national debt, meanwhile, has increased eighty-six-fold since 1970. It currently stands at 119% of GDP and has been above 100% since 2013.

The point: if the public were to demand meaningful changes in long-standing spending and debt trends, it would require a long-standing bi-partisan effort.

References: Actalent's September 2023 Labor Market & Economy Report synthesizes information from a variety of sources including the United States Bureau of Labor Statistics survey results, Lightcast (formerly Emsi-Burning Glass), media reports, industry intelligence, company earnings reports, and external labor market data. The full set of data and references are included as a companion to this article.

If you'd like more information on the data presented, or have questions about the information provided in this report, please contact our team at: content@actalentservices.com.